Affine growth of insurance premiums

Insurance premiums are modelled using the log-normal, Pareto, Gamma and Weibull distributions.

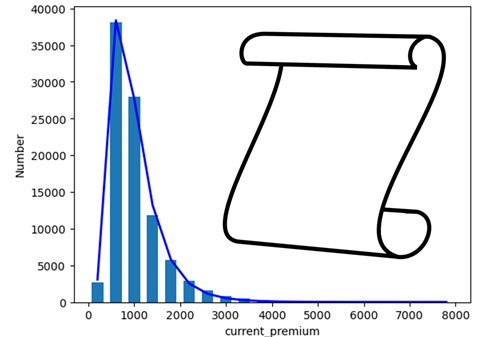

Coin flips with offset returns are approximated by the normal distribution, linear returns by the log-normal and affine returns seem to be approximated by an appropriately scaled logit-normal distribution. A good fit for car insurance is performed by this latter distribution. Perhaps because, for some cases at least, affine returns result in power law tails. Further details for car insurance premiums in the USA are contained in a pre-print on GitHub.